The operational costs of managing and maintaining a professional trading platform and the capital investment required to stand up the necessary infrastructure to support such a platform are substantial. This is particularly true for our TTNET™ hosting service, which provides the expansive functionality and robust performance of TT software along with global reach that spans the world’s major financial markets.

The TTNET global distribution network

The value proposition for customers of TTNET is the transfer of a significant portion of the aforementioned costs and risks to TT, while at the same time procuring higher quality services with lower overall costs than they could do on their own. It’s a similar value proposition of most service providers across all industries.

Our clients who utilize TTNET tell us they prefer our hosting services because it combines the advantages of our world-class, professional trading software platform with the advantages of a highly available, purpose-built infrastructure. An infrastructure deliberately tailored to meet the needs of professional traders, with attributes that include bare-metal computing performance, dedicated and performant connectivity options, and hosting proximity to, or even co-location with, major trading venues and other financial markets partners.

Providing these benefits, though, comes at a cost premium over more general-purpose IT hosting venues. And while we believe these benefits are in the best interest of our end users and worth a premium over lower-cost alternatives, we don’t believe our current implementation, execution and standard service offerings are as efficient or relevant as they could be, irrespective of the constraints of our current software platform. In short, there is room for improvement in both cost and quality.

The prominence of cloud computing in mainstream IT is accelerating the maturation of many IT technologies, and it is leading to better tools for automation and service deployment. But it’s also helping to dispel many industry misconceptions about the security, reliability and performance around three fundamental technologies of “the cloud”: multi-tenancy, virtualization and Internet connectivity—three fundamental technologies that are also fundamental cloud tenets because they directly impact scalability (and consequently cost).

Like all technologies, cloud technologies have their own challenges and limitations. But when applied intelligently and to the right problems, they are viable and cost-effective tools, even for our industry (see: NASDAQ and NYSE Technologies).

Those familiar with TTNET know that we’ve been leveraging many tenets of the cloud for a while now. In retrospect, TTNET is effectively a private cloud and has been since its inception. And while we plan to leverage cloud paradigms, cloud technologies, and even private and public services extensively in our next-generation platform, we’re not waiting for it to arrive before we take advantage of changing perceptions and extend our use of fundamental cloud tenets.

For example…

Historically, TT has only offered dedicated broker environments—meaning an end user in TTNET could only trade through one broker if he had a single X_TRADER® screen. But soon, TT will begin offering MultiBroker service to TTNET clients through a multi-tenant version of TT’s futures execution platform.

Designed as a single execution environment for traders supported by multiple brokers, MultiBroker is TT’s first foray into offering a true application-level, multi-tenant service. Multi-tenancy is a concept that can be applied to any layer of the IT service stack, from the physical layer of shared data center facilities (e.g., power, space and cooling) all the way up to the application layer serving user transactions. Typically, the further up the stack a service provider goes, the greater economies of scale that can be achieved. With MultiBroker, we are going way up the stack.

In addition to the commercial benefits MultiBroker will bring to our client base, its multi-tenant design will greatly enhance the scalability and efficiency of this service offering for both our customers and end users. And now, with the majority of our platform supporting multi-core technology, even greater scale can be achieved while maintaining competitive execution latency and efficient throughput scalability.

Our customers and end users who continue to utilize our original single-tenant hosting option in TTNET will not be left behind, as we are looking at improvements there as well. Today, TTNET uses virtualization technology and tools to support a number of management systems, but only for a very small percentage of trading-related applications, and only where functionality is out of the trade execution data path. Going forward, we plan to leverage virtualization technologies to support mainline trading applications in failover and disaster recovery situations where availability is paramount, but where some compromise in performance is acceptable. But even in the case of failover, by retaining the host’s proximity to the trading venue, we anticipate better performance than we offer today.

Finally, as our customers become more comfortable utilizing secure Internet connectivity, we are looking to transition more leased connections to the Internet. For example, we are evaluating the use of Internet as a backup connectivity option to dedicated private-line circuits without restrictions. This would result in lower connectivity costs to TTNET for our broker firms and end users. Additionally, while TT continues to expand and mature its Strategy Engine (SE) server-based execution solutions, including Autospreader SE, Synthetic SE and Algo SE, we expect more users to connect to TTNET directly via the Internet. As a consequence, we anticipate growing demand for lower-cost back-office connectivity options that offer “Internet-like” connectivity, but over a private cloud.

Look for more insights and perspectives on TTNET in my next blog. Thanks for reading.

Note: If you’re not familiar with X_STUDY®, I encourage you to review the X_STUDY materials on our website. You’ll gain a solid understanding of this trader-centric charting application, which is fully integrated with TT’s X_TRADER® platform and provided to all X_TRADER users at no additional cost.

As the product manager for X_STUDY, TT’s charting and analytics application, I’d like to talk about constant volume bars. Constant volume bars build bars based on fixed volume instead of fixed time. There are several advantages to constant volume bars when compared to time-based bars.

Shorter time-based bars, like one-minute and five-minute bars, are great during the day when there are many market participants and the market tempo is fast. When market tempo slows and price action begins to consolidate, shorter time-based bars will continue generating bars as time passes. Too many of these time-based bars will inevitably flatten out your analytics, which can then generate whipsawed losing trades or take you out of a good trade.

A Case for Constant Volume Bars

A constant volume bar conforms to the market’s tempo. As the market tempo slows, so will the formation of new bars. As the tempo increases, so will the number of bars created. Volume bars are ideal for when events happen in the marketplace, too. For example, the release of an economic event at 1:15 can leave your five-minute bar waiting until 1:20, while the volume bars have already created four new bars in that five-minute window. These four faster-responding volume bars give your strategy more opportunity to react to the event that has just occurred in the market.

Likewise, who needs 12 five-minute bars from 12:15 to 1:15 before that economic number comes out when volume is light? Your analytics will be flat with time-based bars and won’t be able to help you make decisions. A volume chart in this same period might only form one bar. The concept of constant volume bars creates an intelligent bar that reacts to the market’s trading volume.

An Example

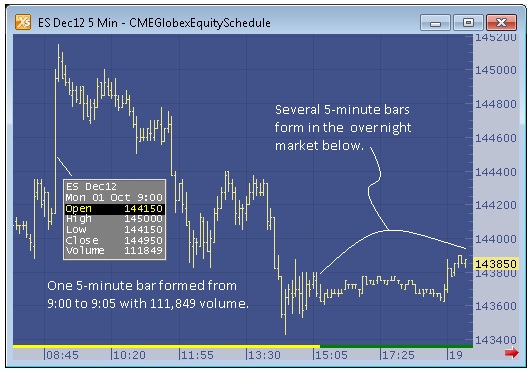

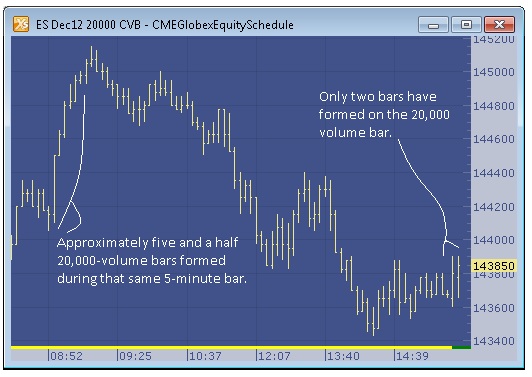

Let’s look at the scenario below, which uses the ES Dec12 contract from earlier this month. Compare a five-minute chart to a 20,000-volume chart. It will show advantages for when markets have both a fast and slow tempo. The five-minute bar chart shows a one-bar spike in the morning hours. The 9:00 to 9:05 a.m. bar in ES spikes to 1450.00. Comparing this bar to the 20,000-volume chart, we can see that approximately 5½ bars were formed on the constant volume bar chart during the same time.

Now look at the overnight market above. Here we can see more than forty bars have formed on the five-minute bar chart. This many bars will cause most technical indicators to flatten out and any automated system to start generating false signals, especially if the technical indicators are using fast values like a simple moving average of six bars. (I actually do not display all the bars here; there are more off to the right of the chart. You can tell this by the little red arrow at the bottom of the five-minute chart.)

The 20,000-volume bar has only produced two bars, with the second one still incomplete. At the time of the screenshot, the bar was only half complete, with around 11,000 volume. This example illustrates the improvement constant volume bars provide in both fast- and slow-moving markets.

In Closing

In my experience, I’ve found that constant volume bars can really improve analytics and help eliminate some of the whipsaws.This isn’t to say time-based charts are unnecessary. In fact, I myself still use time-based charts in much of my analysis. I don’t think I could give up daily charts; they are just too ingrained in my analysis. Rather, I’m simply suggesting that you might gain a little edge by looking at a combination of volume-based and time-based charts.Until next time, plan the trade and trade the plan.

Tags: Charting

More than two years after the Dodd–Frank Act was passed, it’s surprising how much still remains unsettled with regard to what new regulations may be implemented and how the industry will be transformed. One of the few changes that seems certain is that over-the-counter (OTC) swaps will move to a centrally cleared model.

What remains to be seen is which model for trading and clearing interest rate swaps will ultimately win out. Will these swaps remain custom OTC contracts traded via a swap execution facility (SEF)? Or will the industry move toward an exchange model where swap-like futures are traded on a designated contract market?

Siding with Futures

It seems more and more as if the futures model will ultimately win out. Exchange-traded interest rate swap futures have margin efficiencies that the OTC model can’t match. A number of strategies that make use of OTC swaps today may no longer be profitable once these swap positions are subject to margin requirements, an issue which the substitution of swap futures for OTC contracts substantially alleviates.

The trend toward either the “swaps as futures” or “futures on swaps” model is noted by research firms such as TABB Group, but is also reinforced by moves the exchanges are making. For example, the Chicago Mercantile Exchange (CME) recently announced plans to list deliverable interest rate swap futures, and IntercontinentalExchange (ICE) is transitioning its OTC energy contracts to futures.

Making the Swap: Eris Exchange on TT

For these reasons, I was very excited last month when we announced our plans to provide connectivity to Eris Exchange. Eris has created products that capture the best of both worlds. Eris contracts are futures, which means they bring with them margin requirements substantially lower than comparable OTC contracts—up to 95 percent lower for accounts with highly correlated positions. At the same time, Eris products are designed to replicate the cash flows of OTC swaps while also allowing for custom coupons, effective dates and maturity dates to be specified, giving firms the ability to tailor the contracts precisely to their needs.

In addition to being an effective vehicle for corporations to hedge their business risks, a number of strategies based on Eris futures can be executed using TT’s suite of server-side execution tools, such as the Autospreader® Strategy Engine (Autospreader SE) or the new ADL™ visual programming platform with Algo Strategy Engine (Algo SE). These include:

- Invoice spreads between the cheapest-to-deliver Chicago Board of Trade (CBOT) or NYSE Liffe U.S. treasury future and an Eris contract with a similar maturity

- Swap spreads between an Eris future and a similar-maturity BrokerTec treasury

- Eurodollar basis trades between Eris futures and CME or NYSE Liffe U.S. Eurodollars

- Swap curve strategies between different Eris maturities, between Eris futures and BrokerTec cash treasuries or between Eris futures and CBOT or NYSE Liffe U.S. interest rate futures

We plan to roll out our support for Eris in two phases. The first phase, due out later this year, will add support for Eris’ IMM dated forward starting swaps, including Eris’ invoice spread leg contract. In phase two, we will add support for the rest of the Eris product suite, including spot starting swap futures.

Learn More

For more information, visit the Eris Exchange page on our website and read the recent news release announcing our plans to connect to Eris.

And if you’ll be attending FIA Expo later this month in Chicago, stop by our booth (#820) on Wednesday, October 31 at 3:30 p.m. to learn more about Eris futures and how you can trade Eris with TT. Free passes to the exhibit hall, compliments of TT, are available here.

Hope to see you at the show!

Tags: Market Access

Back in 2010, Wired columnist Clive Thompson argued that it’s time for all of us—not just software engineers—to learn how to program software1. It’s been nearly two years since that article was written, but I believe it’s still as relevant today as it was then.

As the product manager responsible for TT’s ADL™ visual programming platform, people often ask me if I think traders can learn to code. I tell them, not only can any trader learn to code, but most traders are already engaged in the mental process of writing a program, whether they know it or not.

As an example, consider a successful point-and-click trader who has a rock-star track record. This trader must know his strategy inside-out and execute it with precision. To be specific, he must have the “pathways” of his strategy mapped out, and, if needed, he should be able to articulate them in an organized and systematic manner.

What makes this trader exceptional, however, is not only the fact that his strategy map depicts the main pathways of logic, but that it also covers the inconspicuous “alleys” or contingencies that can arise in the market. The most successful traders consider the “what ifs” and are prepared with maneuvers to deal with such contingencies.

Continue Reading →

Tags: Algos & Spread Trading

By way of introduction, my role at TT has involved me in a number of strategic initiatives including proximity trading, synthetic orders, Financial Information eXchange (FIX) protocol and application programming interfaces (APIs).

Most recently I’ve been holding discussions with a variety of firms to further enhance the capabilities of our system for buy-side traders and portfolio managers. In this role, I’ve had the pleasure of speaking with some key players in the buy-side community.

Of course, the term “buy side” itself refers to a fairly wide swath of business models, ranging from asset managers to hedge funds. But despite the breadth of the buy side as a whole, a growing number of buy-side users is demanding the option of a high-touch capability in a world otherwise driven toward low-latency, low-touch trading.

All the World’s a Stage

Staged Orders in X_TRADER®

Order staging, which involves the creation of staged or “care” orders, is in some ways an idea that’s as old as agency trading itself. Although they weren’t called care orders at first, care orders started as a voice call to a sell-side trader over telephones and squawk boxes. As technology marched forward, the vehicles for submitting care orders evolved to include faxes, followed by emails and instant messages.

Continue Reading →

Tags: Trade Execution